Content

The most important question on my mind during the financial services outlook was: "In your analysis of insurers and sovereign risk, climate stress is often expressed through disasters like floods or droughts. But how much attention do financial institutions currently give to chronic resource degradation as opposed to acute shocks and do you expect that to materially affect underwriting, sovereign spreads, or bank balance sheets over the next 3–5 years?"

To which the analysts highlighted that while financial institutions are increasingly equipped to respond to acute shocks, chronic resource degradation - particularly water scarcity - remains under-recognized in financial risk assessments, potentially creating hidden vulnerabilities on balance sheets. The insurance sector, meanwhile, faces pressure from slower premium growth, trade disruptions, and escalating climate risks, prompting greater focus on parametric insurance solutions and public–private partnerships to manage emerging exposures.

A key takeaway was that chronic resource stress is moving from an environmental concern to a material financial risk that institutions can no longer afford to overlook.

Implications for water finance

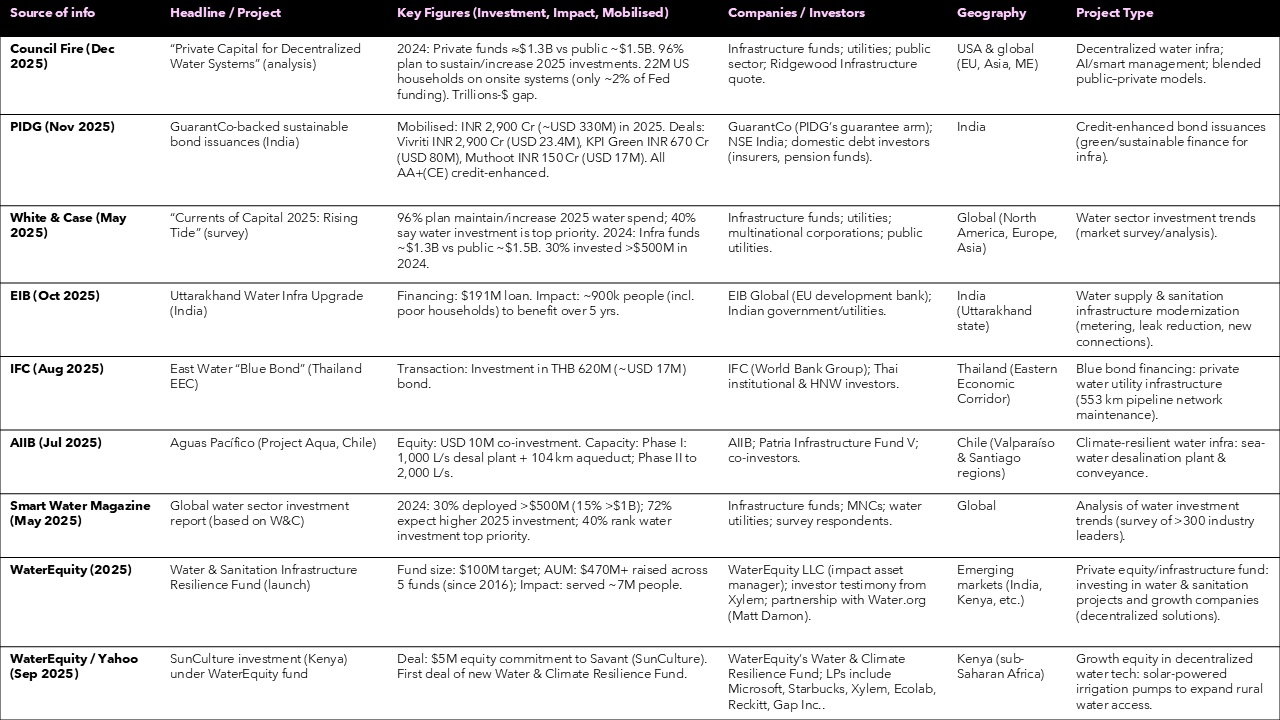

The outlook warns of tighter interest margins and fragmented regulation ahead. In practice, this means higher borrowing costs and uneven funding availability for infrastructure projects, including water systems. To fill the gap, private capital is stepping in: one study finds private funds invested about $1.3 billion in water projects in 2024 – nearly matching the public sector’s $1.5 billion. This shift reflects a “growing collaboration” between public and private finance for water. At the same time, risk assessment must evolve: lenders and insurers will increasingly price in water-specific risks (e.g. drought, quality) as part of credit models.

Caelra helps financial institutions and project sponsors understand how water-related physical, regulatory, and delivery risks translate into project-level financial exposure. Our work informs capital structuring decisions, including the use of blended finance, alternative debt instruments, and risk-sharing mechanisms with development finance institutions and impact investors.

Regulatory shifts affecting water finance

Regulation is both diverging and tightening. Our analysis notes an era of fragmented regulation and some deregulation in finance, which could loosen controls on financial products but also create uneven standards. Conversely, sustainability rules are becoming stricter: for example, the EU’s Sustainable Finance Disclosure Regulation (SFDR) is actively pushing asset managers into “water security” investments. Sovereign “blue bonds” illustrate this trend – Indonesia’s blue-labelled bond issuance jumped to $987 million in 2024 to fund water and sanitation projects. Moreover, surveys show 90% of investors now believe water stewardship should be central to ESG reporting, and 75% already integrate water metrics into their sustainability strategies. (Currently, however, many ESG frameworks lack detailed water indicators.)

Caelra tracks the evolution of sustainability and disclosure regimes and assesses their implications for water-dependent assets and portfolios. We support institutions in navigating emerging expectations around water risk disclosure, impact metrics, and regulatory engagement- particularly where existing ESG frameworks fall short of capturing physical resource constraints.

Climate and insurance risks for water assets

Climate-driven disasters are straining insurers. Insured losses from natural catastrophes now exceed $100 billion per year, even before accounting for uncovered losses. Underwriting is tightening accordingly – regulators are insisting that climate risk be explicitly incorporated into insurance pricing and risk models. Water assets face acute flood and drought exposure: for instance, U.S. floods from 2010–2023 caused $144 billion in damages but only $50 billion was insured (35% coverage). A single Texas flood in 2025 generated about $18–22 billion in losses, most of which were uninsured. These protection gaps signal that many water-related projects (reservoirs, irrigation, utilities) may struggle to find affordable coverage or may require special products (e.g. parametric insurance or catastrophe bonds).

Caelra analyses how climate-driven water risks affect asset valuation, insurability, and long-term financial performance. Our work highlights where conventional risk models underestimate chronic exposure and where resilience investments materially alter insurance availability, pricing, and capital allocation.

Digital finance and water infrastructure (tokenization)

The rise of digital finance offers new funding channels for water projects. The outlook highlights evolving digital financial infrastructure (stablecoins, tokenized deposits) in 2026. In the water sector, real-world asset (RWA) tokenization is already emerging as a solution. For example, blockchain platforms are “tokenizing ownership stakes in water systems” – a pilot in Jakarta tokenized eight treatment facilities using a local stablecoin. Tokenization enables fractional ownership, liquidity and global participation in infrastructure funding. Smart contracts and blockchain transparency can streamline due diligence and allow retail as well as institutional investors to fund local water projects.

Caelra examines the potential role of digital finance and emerging financial infrastructure in mobilising capital for water and climate-resilient assets. This includes assessing regulatory readiness, financial viability, and risk implications of tokenised instruments and platform-based funding models across jurisdictions.

Consolidation vs. decentralization in water finance

Water finance is moving in two directions. Large utilities and funds are consolidating capital, while localized solutions are on the rise. Private infrastructure funds are now investing heavily in “distributed” water systems. In fact, private funding ($1.3 b) nearly equaled public funding ($1.5 b) for water projects in 2024 (see chart above). This shift “signals a departure from traditional muni bonds” toward partnerships and hybrid public–private models. At the same time, many small systems remain undercapitalized: e.g. decentralized onsite wastewater systems serve ~22 million U.S. homes (~20% of households) but have historically received only ~2% of federal funding. This gap suggests opportunities for local finance solutions (community bonds, DeFi-like platforms) to fund regionally important water assets.

Caelra provides comparative insight into how capital mobilisation strategies differ between large-scale infrastructure platforms and decentralised, community-level water systems. Our work helps institutions understand where consolidation unlocks efficiencies and where decentralised models are necessary to reach underserved or high-risk contexts.

Macroeconomic and geopolitical context

Water finance does not exist in a vacuum. Geopolitically, water scarcity is becoming a strategic risk – EY notes that nearly 4 billion people face severe water stress annually, and water rights are “causing and exacerbating political conflicts” in 2026. This can affect project viability (e.g. transboundary water projects may face new tensions). Macroeconomically, record global debt (235% of GDP) and heavy sovereign borrowing are raising interest costs and “crowding out private investment”. That means less fiscal room for water infrastructure and higher financing hurdles. Trade and supply-chain tensions (tariffs, commodity controls) are also a factor: insurers warn that tariffs and supply disruptions are already driving up costs and coverage gaps. In sum, geopolitical shocks (conflict, trade wars, climate policy) could swiftly alter water access and project risk.

Caelra assesses how geopolitical dynamics, trade disruptions, and climate-related instability shape the risk profile of water investments across regions. We support strategic decision-making by highlighting where water infrastructure intersects with national security, fiscal exposure, and sovereign risk considerations.